This week the price of oil was negative! Yes, a negative price! How is it even possible to be paid to buy something? By the end of this post, not only will you understand what happened in the oil market, but you will have a good grasp of how the prices work in the futures market, and what are contango and normal backwardation.

You can also watch my video “CONTANGO AND BACKWARDATION EXPLAINED, Forward and Futures Prices, and the Oil Price Crash” on my YouTube’s channel. Check it out!

Spot markets and term contracts

The April 2020 oil price crash is a direct consequence of futures trading. Commodities, and other financial instruments, may trade both on a spot market, for immediate delivery, and on a futures market where the payment and delivery will occur at a distant date.

For example, the spot market for crude oil and refined products consists of one-off transactions paid and delivered in the near term. Overall, for oil, it is a small market, and the majority of transactions occur under term contracts: forwards and futures.

Forwards and futures both require the payment and delivery of the underlying product at a future date, but forwards are over-the-counter instruments, two parties decide together what are the mutually attractive terms of the exchange. In contrast, futures contracts are standardized and traded on exchanges, like the CME or the CBOE.

It is an old invention. The Chicago Board of Trade was founded in April 1848 as a cash market, another name for the spot market, to trade grain. Nearly immediately, forward or “to-arrive” contracts began trading. And in 1858, the first standardized futures contracts appeared. These financial instruments were developed to help farmers to sell their future production and hedge themselves against a potential price decline.

Since forwards and futures are the same kinds of financial instruments, in the rest of the post, I will talk only about futures, but everything also applies to forwards.

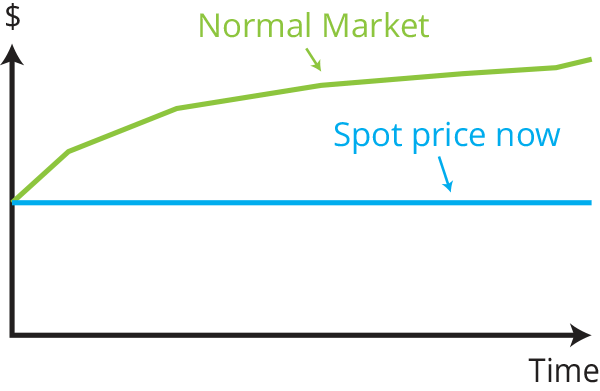

Normal and inverted markets

One question you may ask is how the futures price of something is determined. The something can be anything: oil, corn, pork bellies, iron, gold, google stock, or the Dow Jones index.

Should the futures price be higher than today’s spot price, or should it be lower? The simple answer is that it depends, but higher futures prices are the most common. The main drivers of the difference between current and futures prices are storage and financing costs. Higher they are, higher is the futures price. When futures prices increase with maturity, it is known as a normal market. Today, despite what happened on April 20, 2020, oil is an example of a normal market.

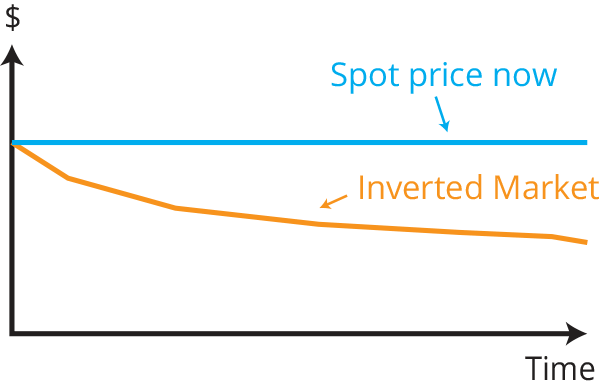

On the other hand, if they decrease with maturity, we have an inverted market.

Futures Prices vs. expected prices

Does it mean that the price we see today for futures contracts represents the expected spot price at the contract maturity? In other words, does the average opinion of all the market participants give us an idea of where the price ultimately will be? What do you think?

If your answer to that question is no, you are right!

To understand why let’s go back to the economic theory. Economists John Maynard Keynes and John Hicks give us an idea of what could be happening. They argued that there are two kinds of market participants: Hedgers and speculators, and their actions determine if prices of futures are above or below the true expected price.

For commodities, hedgers are usually the producers. They do not want to lose money if the commodity prices fell. However, in the aviation sector, hedging means protecting against oil prices going up, not going down. For stocks, hedgers are investors who want to protect their portfolio.

And we have speculators, who, on average, take the opposite side of hedgers. They are accepting to take a risk with their money, but they are expecting to be compensated for that.

To be protected against a price drop, hedgers sell futures contracts, locking-in the price at which they will sell their products. On the contrary, to be protected against a price increase, hedgers buy futures contracts, locking-in the cost at which they will buy something. And since hedging is akin to purchase insurance, hedgers are accepting to lose money on their hedge to be protected.

Hedgers want protection against falling prices:

— Hedgers sell futures

— Speculators buy futures

Hedgers want protection against rising prices:

— Hedgers buy futures

— Speculators sell futures

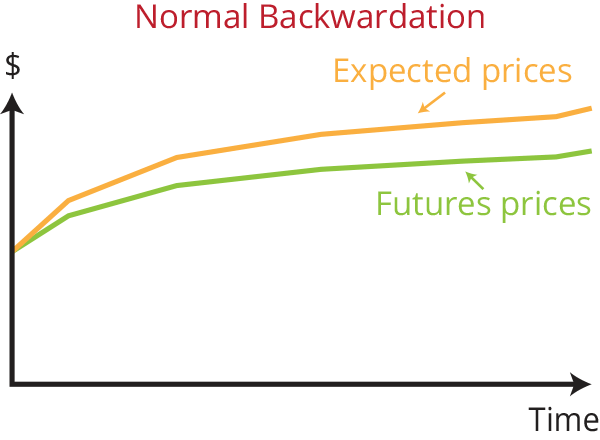

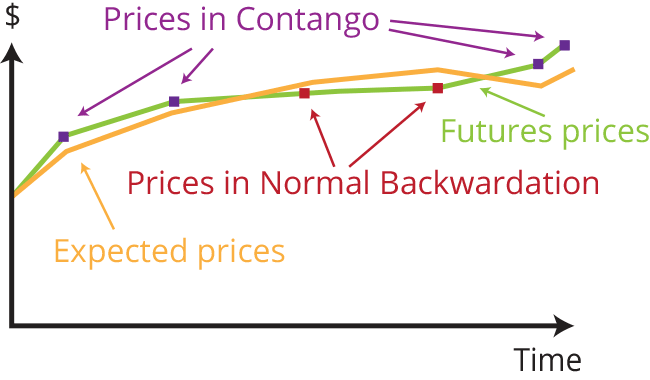

Normal backwardation

If hedgers, on average, want to be protected against a decline in price, and speculators, on average, are providing that protection, the real expected price must then be higher than the price of the futures. Why? Because speculators expect to buy low and sell high, and hedgers agree with that. It is called a “normal backwardation” or simply “backwardation.”

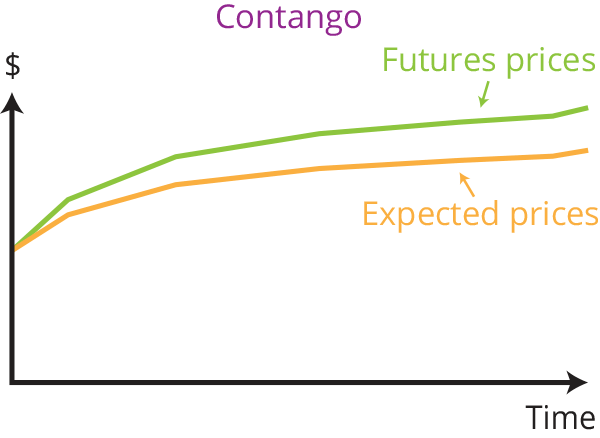

Contango

On the contrary, if hedgers, on average, want to be protected against soaring prices, the real expected price must then be lower than the price of the futures. Speculators expect to sell high and buy low ultimately. And hedgers got the protection they needed. The prices are in “contango.”

For example, the VIX index, often referred to as the fear index, has its futures usually in contango. Portfolio managers buying VIX futures to protect their portfolio are paying in effect large sums to VIX sellers for that. Because selling VIX futures is a highly risky proposition.

Contango and normal backwardation

So contango and normal backwardation have nothing to do with the prices of futures compared to the spot price, but futures prices compared to expected prices. I have to say that I heard professional investors being confused about that, so if you got this right, you are now one step ahead!

The oil price crash (April 2020)

Now, what happened to oil prices on April 20, 2020? Futures prices became negative, and buyers were paid to get oil.

As bizarre as it is, it is entirely rational. Energy demand is spiraling down. In consequence, it means that storage capacity is scarce because oil is not moving, and existing storage is nearly full. Also, there is one aspect of commodity futures you must be aware of, especially if you intend to trade them. Most commodity futures contracts require physical delivery. Imagine you are a New York investment banker, or a fund manager, trading oil contracts, and you have a net buying position when trading for that contract terminates. Can you imagine having a delivery? An oil supertanker waiting for you on the Hudson River? I am joking here because it will not be on the Hudson River, though you would have to take delivery of your oil in Oklahoma.

Banks, funds, and speculators, in general, never want to do that, and they close their positions before the contract matures. But in April 2020, there is no demand, and no storage available in Oklahoma. Therefore they paid money to offload their long futures contracts and took huge losses.

However, don’t jump to any conclusion here. It is not the end of the world. And, we are not on the brink of a financial Armageddon. OPEC countries and Russia agreed to slash their oil production. And the oil markets returned to a regular situation in the following days. Oil-producing companies will suffer from low oil prices, but it is another story.

I understand why negative oil prices made to the headlines. However, as an investor, you should always stay calm and analyze the situation.

Question of the day: What do you think about the influence of hedgers and speculators in the futures market?

Share your thoughts, and thank you!

Don’t forget to share this post. You can also subscribe to my YouTube’s channel! Thank you so much for your support!

Question of the day:

What do you think about the influence of hedgers and speculators in the futures market?

Recent Comments